2026 is going to reward Canadian deep tech founders who can commercialize. Full stop. I spend my time with founders, engineers, investors, and operators through Fello Agency and Fello Foundry. We work across AI, quantum, XR, advanced manufacturing, medtech, and defence. We built Fello from the ground up without venture money, so I look at this market through a very simple lens. Can this company turn serious science into real demand? That question is getting sharper. Capital is tighter. Buyers are more skeptical. Investors can spot bullshit a mile away. If you are building in Canada right now, especially from Series A to C, you need to understand what the market is actually rewarding.

Key Takeaways

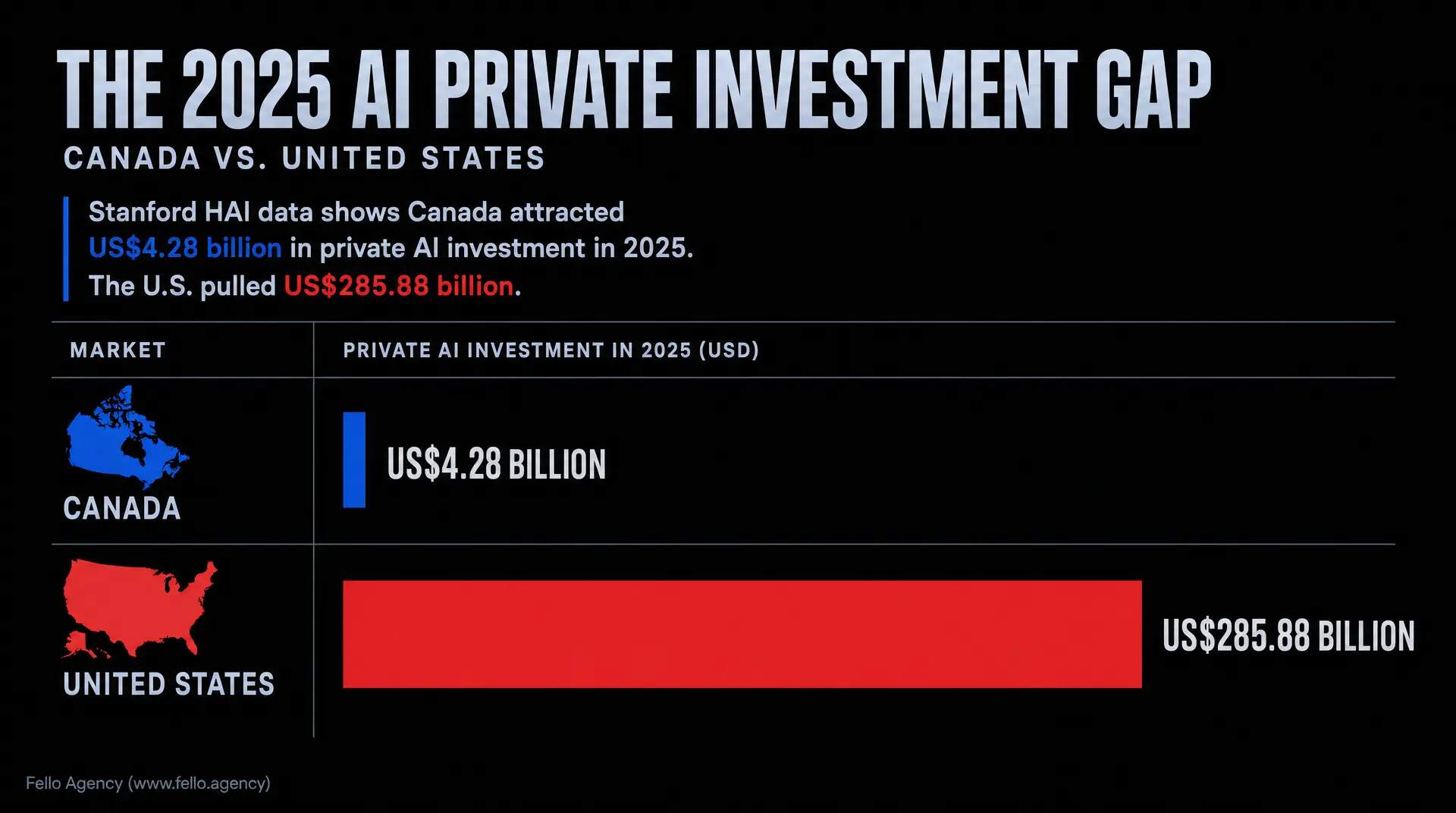

Stanford HAI data reveals Canada attracted 4.28 billion dollars in private AI investment in 2025 compared to 285.88 billion dollars in the United States, making direct competition in frontier AI models financially difficult.

Only 51% of Ontario companies with an artificial intelligence vision implemented an enterprise-wide strategy in 2024-25, demonstrating a severe gap between technical interest and commercial execution.

Canada's 2026 Defence Industrial Strategy mandates that 70% of defense acquisitions go to Canadian firms, opening 180 billion dollars in procurement opportunities for dual-use technology founders.

Centering brand storytelling around applied scientists rather than product specifications drove an 80% increase in website traffic in six weeks for pre-revenue deep tech firm Nord Quantique.

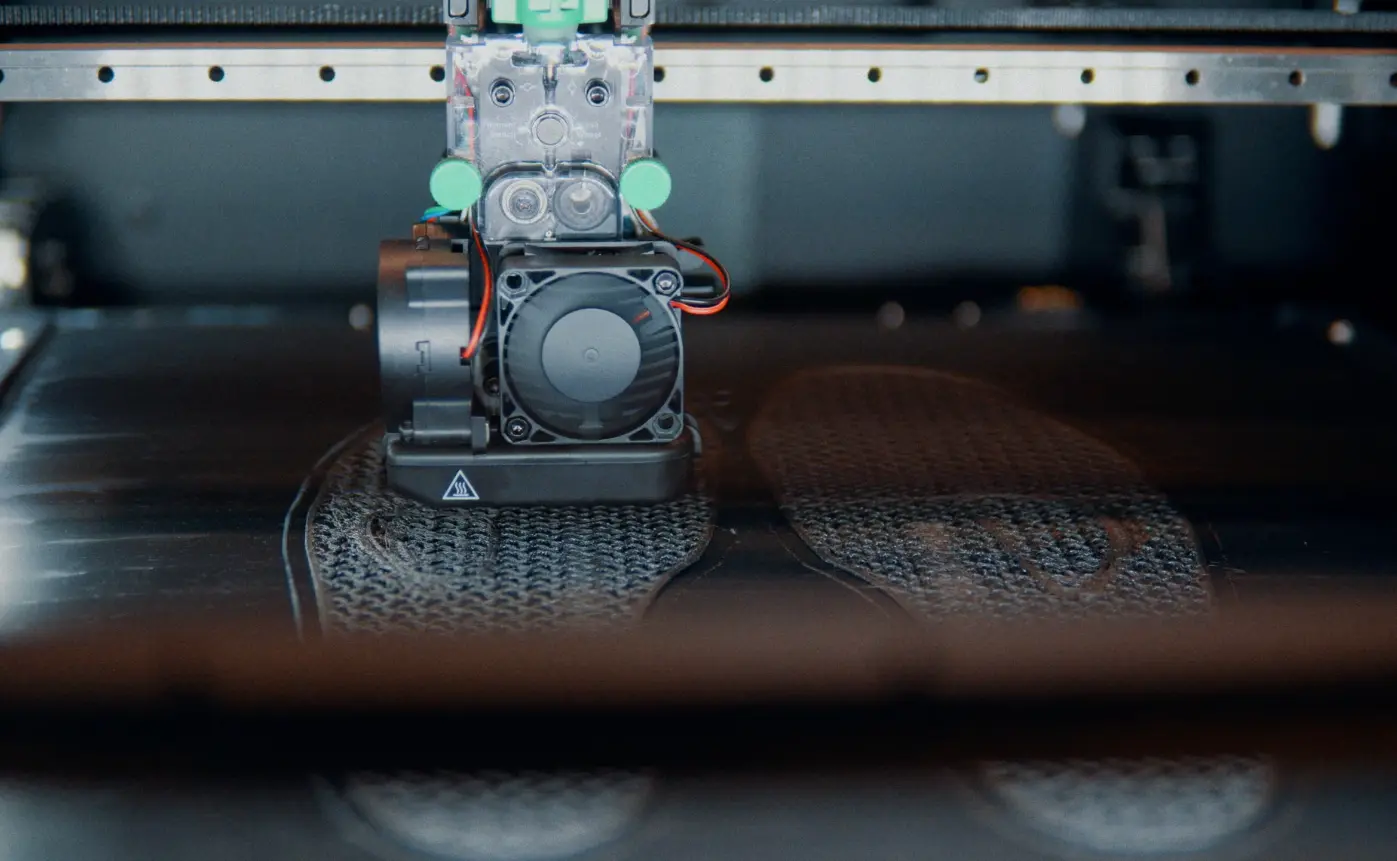

Shifting marketing focus from hardware specifications to specific orthotics business workflows increased inbound leads by 25% and booked meetings by 15% for Mosaic Manufacturing.

The Canadian government allowed 4.6 billion dollars across 24,160 Scientific Research and Experimental Development claims in 2025-26, providing non-dilutive capital that enables founders to delay early United States expansion.

Canada Has the Brains. the Gap Is Conversion.

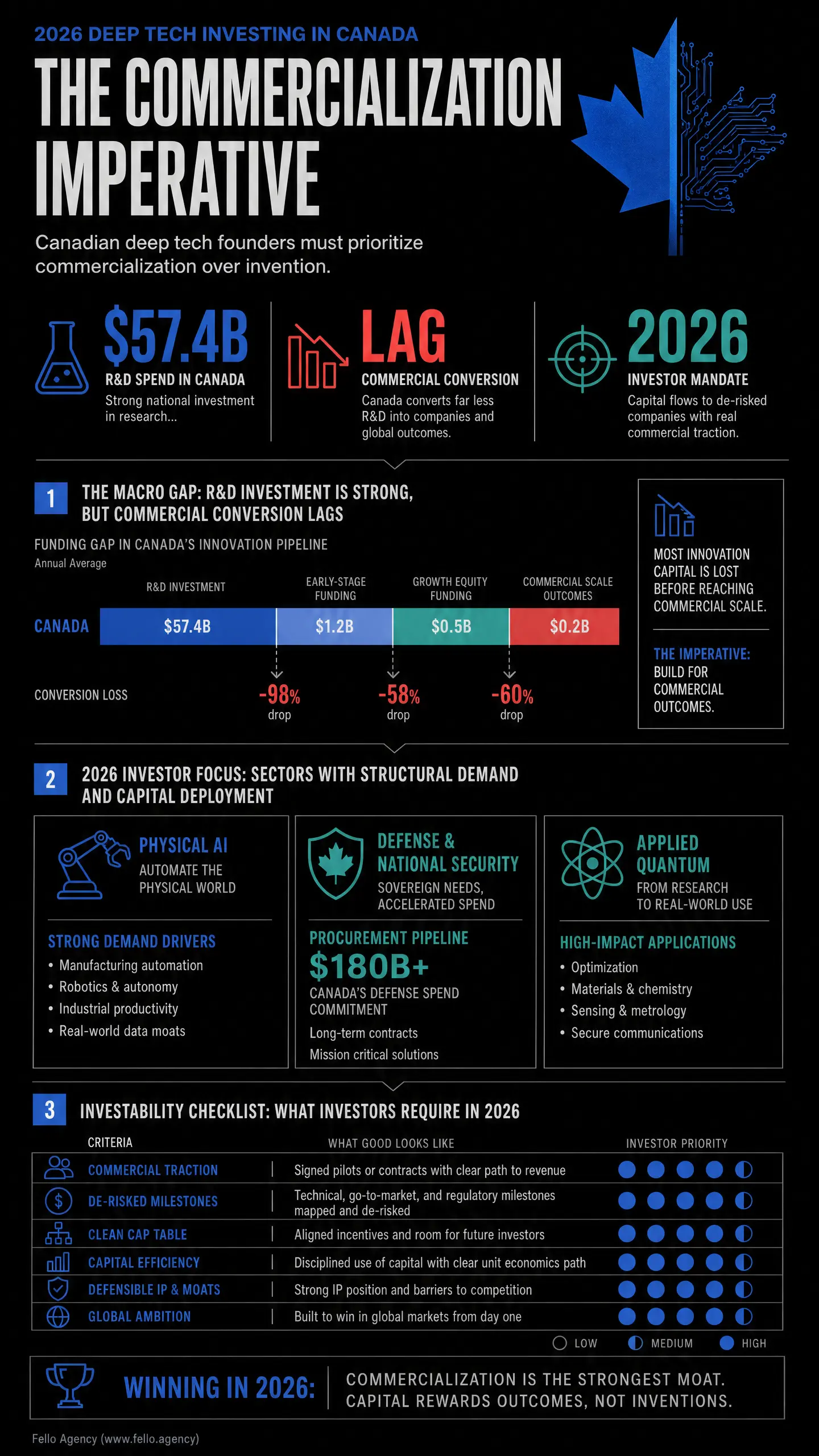

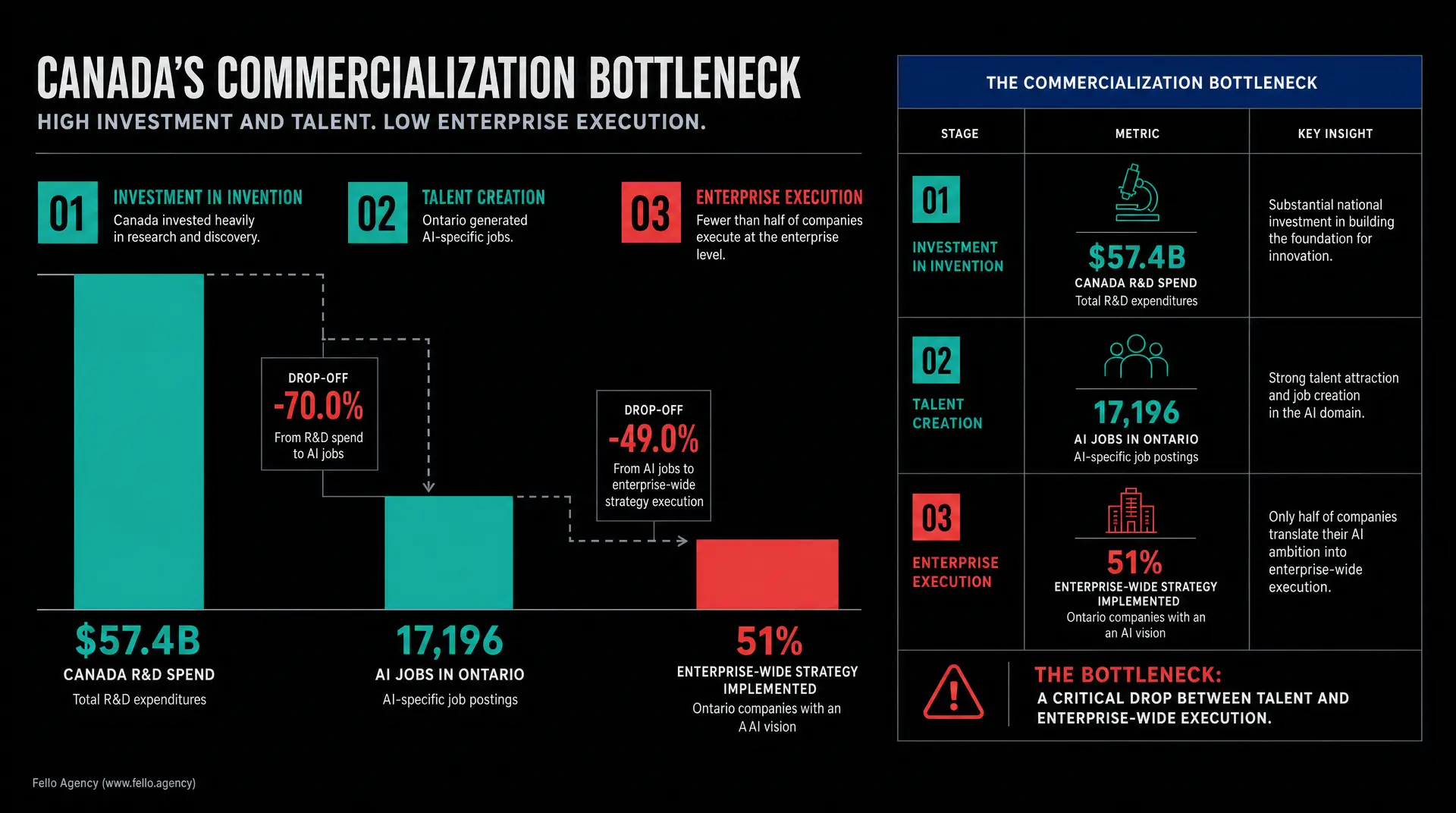

Canada still puts serious money into invention. In 2023, the country spent $57.4 billion on R&.D. The labs are here. The researchers are here. The technical talent is here. But the structural picture is still weak. OECD data shows Canada's R&D intensity was only about 1.8% of GDP in 2023. That sits below the OECD average, below the U.S., and nowhere near Korea. So yes, we know how to invent. We still struggle to turn invention into companies that dominate markets. Ontario shows both sides of that story. Vector Institute reports that Ontario created 17,196 AI jobs in 2024-25, retained 39,327 more, added 70 new AI companies, attracted 27 relocating ones, and pulled in $2.6 billion CAD in VC for Ontario-based AI firms. That is a real ecosystem. There is no question about that. The problem is the commercialization layer. Only 51% of Ontario companies with an AI vision had an enterprise-wide AI strategy implemented or in development in 2024-25. That tells you exactly where we still get stuck. We are good at interest. We are weaker at execution.

The market is still moving fast underneath that. Statistics Canada shows Canadian business AI adoption went from 6.1% in Q2 2024 to 19.2% in Q2 2026. Robotics tells a similar story. Statistics Canada found robotics adopters made up only 2.0% of businesses, but accounted for 11.5% of total revenue and were far more innovative than non-adopters. That is a huge signal. Adoption is still early, but the upside is very real. The talent story is shifting too. Demand for core AI skills rose 37% from 2018 to 2023, while demand for peripheral AI skills fell sharply. The market wants specialists now. At the same time, startups here are still losing senior talent to bigger offers in Canada and the U.S.

That is why I keep saying Canada is an amazing place to build and still a frustrating place to go to market. Toronto invented deep tech learning, but a lot of the commercial upside still gets captured elsewhere. Too many AI startups here still get shaped around a bank acquisition because the big five banks act like the de facto VC plus exit ecosystem. That shrinks ambition early. And speed is still a problem. A lot of Canadian companies want to move in months when they should be moving in weeks. You don't wanna be moving slow in tech, you're gonna get killed.

Where the Money Is Actually Going

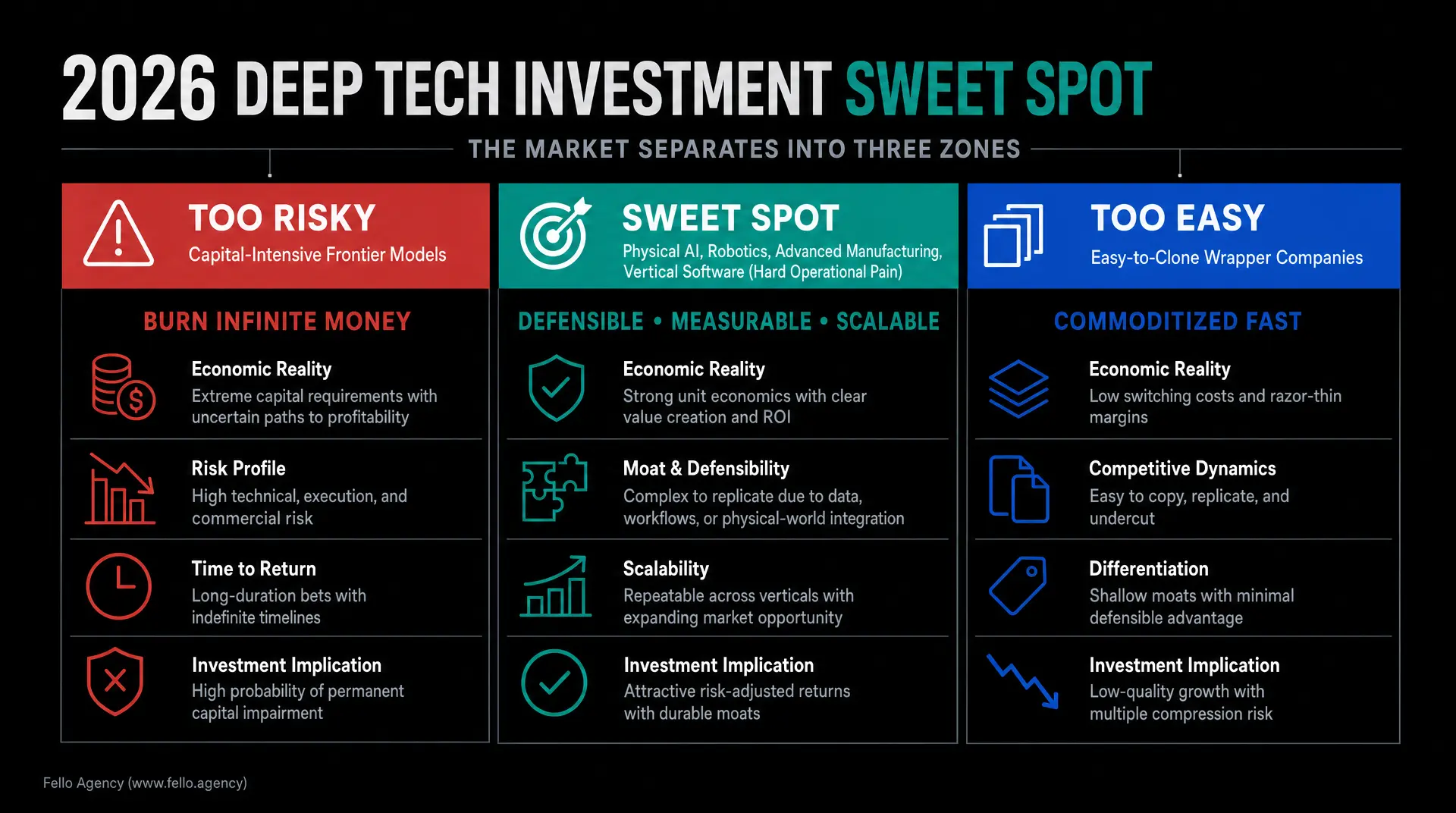

A lot of founders still talk about AI as if the market is one giant open field. It isn't. The money is separating real platform plays from wrapper companies very quickly now. Stanford reported that over 90% of notable frontier AI models in 2025 were produced by industry. That matters. Frontier AI is now a capital game, an infrastructure game, and a commercialization game. It is not just a lab game anymore.

And the money gap is massive. Stanford HAI data shows Canada attracted US$4.28 billion in private AI investment in 2025. The U.S. pulled US$285.88 billion. China pulled US$12.41 billion. So if your plan is to go head-to-head with the biggest model labs, you need to be brutally honest about the capital math. On the other side, if your company is very cheap to build and easy to clone, investors are going to worry that you are just another wrapper. That is a bad place to live too. One end of the market burns infinite money. The other gets commoditized fast.

The sweet spot in 2026 sits in the middle. I like physical AI. I like computer vision. I like robotics, semiconductors, advanced manufacturing, diagnostics, and vertical software tied to hard operational pain. I like products built around concentrated data and very specific use cases. That is where you can still build a moat. The easiest analogy is electricity. The first wave gives the buyer a little efficiency. Fine. The real upside comes when the whole workflow gets redesigned around the technology. Investors are looking for companies that can drive that second phase.

Geopolitics is the new spec sheet too. Canada's 2026 Defence Industrial Strategy lays out $180 billion in defence procurement opportunities and $290 billion in defence-related capital investment over the next 10 years. It also targets 70% of defence acquisitions going to Canadian firms. That is a serious demand signal for dual-use and hard tech founders. Global defence demand is moving the same way. NATO estimated Canada's defence spending at 2.01% of GDP in 2025, while total NATO defence spending reached US$1.405 trillion. Nations are becoming first buyers in categories where private buyers used to move too slowly. That can pull hardware forward on a venture timeline. I still take quantum seriously too. Canada has $360 million in dedicated quantum funding. That is a real foundation. But in quantum, maybe more than anywhere else, honesty about stage matters. Investors can handle early. They do not like fantasy.

What Makes a Company Investable

Pre-Seed and Seed

At the earliest stage, I still want serious science. Deep subject matter expertise matters a lot. But I also want a company, not a lab with a logo.

The ideal setup is still a strong technical founder plus a strong commercial founder. If you do not have both, then the technical founder needs to be comfortable talking to customers directly. That shift is huge. You stop optimizing for the next paper and start optimizing for the next milestone that de-risks the company. I see this problem all the time. Technical founders can explain every layer of the stack and still struggle to answer the only question that matters in the room. Why does a buyer change behavior because of this?

In deep tech, most companies are asking the market to change operations to either make more money or save more money. If you cannot say that clearly, the risk goes up fast. Investors feel it immediately.

Early rounds should buy you a real de-risking event. Customer validation. Partner validation. Regulatory validation. A meaningful technical milestone tied to a commercial path. Raise enough to hit something that changes the story. If you raise too little, you just stay uncertain for another year.

Series a and Beyond

By Series A, the standard gets tighter. I think investors will take tech risk or market risk. They will not happily take both.

You should know who buys, what they pay, where you fit, what performance threshold matters, and what the margin profile can look like. You can still be pre-revenue. You cannot still be fuzzy. If your pitch still sounds like the next research breakthrough instead of the next business, people feel that right away.

This shows up a lot in robotics and hardware. Companies get stuck in pilot purgatory and blame the product. A lot of the time, the real problem is trust. The internal champion cannot explain the rollout upstairs. The company has not built the boardroom narrative that makes scale feel safe. Investors notice that.

If your sales calls are full of explaining what the company is not, you probably have a positioning problem baked into the brand. That gets expensive very quickly.

Team and Cap Table Structure

Team structure matters too. In deep tech, I like multiple founders more than solo founders. I like equity splits that reflect actual time commitment. If an academic founder is part-time, the equity should look part-time.

Keep university ownership tight. Keep the legal structure clean. Investors hate cleanup stories.

Be careful with weird side structures too. Consulting company on one side. IP holdco on the other. Royalty hooks floating around. Venture studios grabbing 40% to 50% before the company is real. All of that slows you down later, and it scares serious capital.

Stay Canadian Early. Cross the Border on Purpose.

Founders ask me all the time when they should move to the U.S. My answer is usually simple. Stay Canadian early if the structure is helping you. Cross the border when there is a real commercial reason.

Canada still has a big advantage in non-dilutive funding. CRA reported 24,160 SR&.ED claims for the 2025-26 period, with $4.6 billion allowed and 59% of credits refundable. NRC IRAP supported 9,187 clients in 2024-25 and backed 13,750 jobs. That is some of the cheapest capital you are going to see after revenue.

Use that while it helps. Keep your CCPC status if it matters. Build with Canadian talent if the talent is here. Then move when the reason is real. U.S. customers. Defence contracts. Access to global capital markets. A specific operator hire. Those are real reasons. Moving because it feels more impressive is not a strategy.

You also need to be honest about exits. CVCA data shows Canadian VC hit CAD $8.0 billion across 571 deals in 2025, but there were only 29 venture-backed exits and zero IPOs. That is a tough backdrop. The TSX is a valuation graveyard for tech. Real winners dual list, or skip the TSX entirely.

Commercialization Now Sits Inside the Investment Thesis

This is where I think a lot of technical founders still leave money on the table. Commercialization is no longer some soft layer you add later. Investors are underwriting it now. Branding in deep tech is authentication. It is the market seeing whether you have professionally validated your own belief in the product. Strong B2B branding is the last moat standing because it reduces perceived risk fast. It helps you skip a level in the sales cycle. You get faster email responses. You get easier first calls. You stop wasting time proving you are real. Your website needs to speak business. Your deck needs to speak business. Your case studies need to speak business. Lead with ROI. Lead with evidence. Lead with what changes for the buyer. A lot of technical founders still lead with features, and that is one of the biggest mistakes they make. If you do not have the runway to teach the entire market a brand-new category, then do not force that on yourself. Work inside a category buyers already understand. You can always expand later. Early on, clarity beats cleverness. I have seen the cost of bad trust signals firsthand. A client lost a deal with Amazon because their visuals were poor. Same room. Same product. Wrong trust signal. If it looks sloppy, people start wondering where else the sloppiness lives.

That is what investors want to see. They want proof that you can translate. They want proof that the company can move from hard science into buyer language without losing credibility. One more thing. Too much polish can hurt you in hard tech. If everything looks like a giant CGI promise and nobody can see the actual work, buyers start thinking vaporware. Show the lab. Show the team. Show the process. If you hide your process, the market will assume you're hiding a flaw. And look, I do not care if you have to subsidize the first deployment. The first real case study is worth a lot. It helps you fundraise. It helps you recruit. It helps you sell. Your future hires are watching too. Great engineers and operators pattern-match hard. If your company still looks like a science project, they will treat it like one. These are still long sales cycles. Six months. Sometimes two years. Human selling still matters. A good technical brief should be useful enough that a buyer can forward it internally and, in many cases, use it for helping write their future RFPs.

Where I Think Smart Money Wins in 2026

I like physical AI a lot. Robotics, computer vision, industrial automation, and software wrapped around real operations all make sense to me. The adoption numbers are still early enough for upside, and the pain is usually obvious to the buyer. I like dual-use and defence even more than a lot of founders are comfortable admitting. The budgets are moving. The demand is real. The trick is knowing that defence marketing is really credibility infrastructure. If you cannot visually show the contract you are trying to land, you are probably not landing it. I like semiconductors and infrastructure when the company understands that time to market, thermal performance, software integration, and supply-chain resilience matter as much as raw benchmarks now. I still like biotech and medtech too, especially when founder credibility is strong and the company knows how to explain the mechanism in plain business language. If you came to me tomorrow and said you were raising, I would start with the story. Get it down to one sentence a non-technical executive can repeat. Then I would push you into customer calls until you know exactly what frustrates the market and why buyers switch. Find out what pisses off your clients the most. After that, I would make you decide whether your next round is really underwriting tech risk or market risk. Then I would clean up the cap table, build one serious proof asset, and fix the credibility layer across the website, deck, and visuals. That is the work. That is how you stop looking like a science project. That is how you start looking fundable. And move fast. Do not disappear into a 90-day audit. Ninety days of diagnosis is eternity. Your competitors will use that same time to ship, tighten the message, build domain authority, and book demos. If your bottleneck is output, own it. Hiring a fractional CMO when you do not have an execution engine is like hiring a head coach for a team with no players.

Final Thought

I am bullish on Canadian deep tech. I am just not bullish on Canadian hesitation.

We already have the science. We already have the talent. The next winners will be the founders who take commercialization as seriously as the invention itself. They will move faster. They will tell the truth about stage. They will build trust early. And they will create companies that people can buy from, invest in, join, and believe in.

Create a business, not a research problem.

Frequently Asked Questions

How do Series A investors view university IP holdcos on a deep tech cap table?

They hate them. Serious capital runs from messy cap tables and weird royalty hooks. If an academic founder is part-time, their equity should reflect that. You need to clean up university ownership and legal structures before raising. Investors want a scalable business, not a complex legal cleanup project.

Is it possible to scale a deep tech hardware company using only non-dilutive funding?

Not at scale. Non-dilutive capital is incredible early on - the CRA allowed $4.6 billion in SR&ED credits recently. Use it to de-risk your science. But scaling advanced hardware requires aggressive venture capital. SR&ED buys you runway. It does not buy you global market dominance.

What metrics do deep tech VCs look for if a company is still pre-revenue?

They underwrite commercial clarity. You can be pre-revenue at Series A, but you cannot be fuzzy. Investors want proof of customer validation, clear margin profiles, and a defined performance threshold. They will take either technology risk or market risk, but they will absolutely not take both.

Why is it so hard to recruit specialized commercial leaders for Canadian AI startups?

Compensation and competition. Demand for core AI skills jumped 37% from 2018 to 2023. We are constantly losing senior talent to massive U.S. offers. To win them, you must offer aggressive equity and prove your science is actually a commercial product, not just a prolonged research project.

Should deep tech founders target the defense sector to accelerate their Series B?

Yes, if your technology is truly dual-use. Governments are now acting as early adopters. With Canada's $180 billion in defense procurement opportunities over 10 years, the demand signal is real. Defense contracts provide the ultimate credibility infrastructure to pull cautious private venture capital off the sidelines.

Your Creative Partner for Innovation That Matters

From advanced tech to transformative healthcare, Fello helps visionary teams shape perception, launch products, and lead industries.

Let’s keep in touch.

Discover more about high-performance web design. Follow us on Linkedin and Instagram.